GLOBAL OVERVIEW KIWIFRUIT

From

| 10 May 2022

Overview of kiwis in the U.S. market, complemented by charts from Agronometrics. Original published on May 6, 2022.

It’s all go in the world of kiwis, as the European season makes way for the New Zealand season, with Zespri at the forefront. The demand for kiwis on many market continues to grow, including in France, where a new French kiwi grower organisation has been set up to benefit from this continued increase in consumption. South Africa also aims to significantly increase it’s domestic production. Although somewhat improved, logistical issues remain an issue for this fruit, which relies on import to many market, causing a back up of European production on both the North and South American markets.

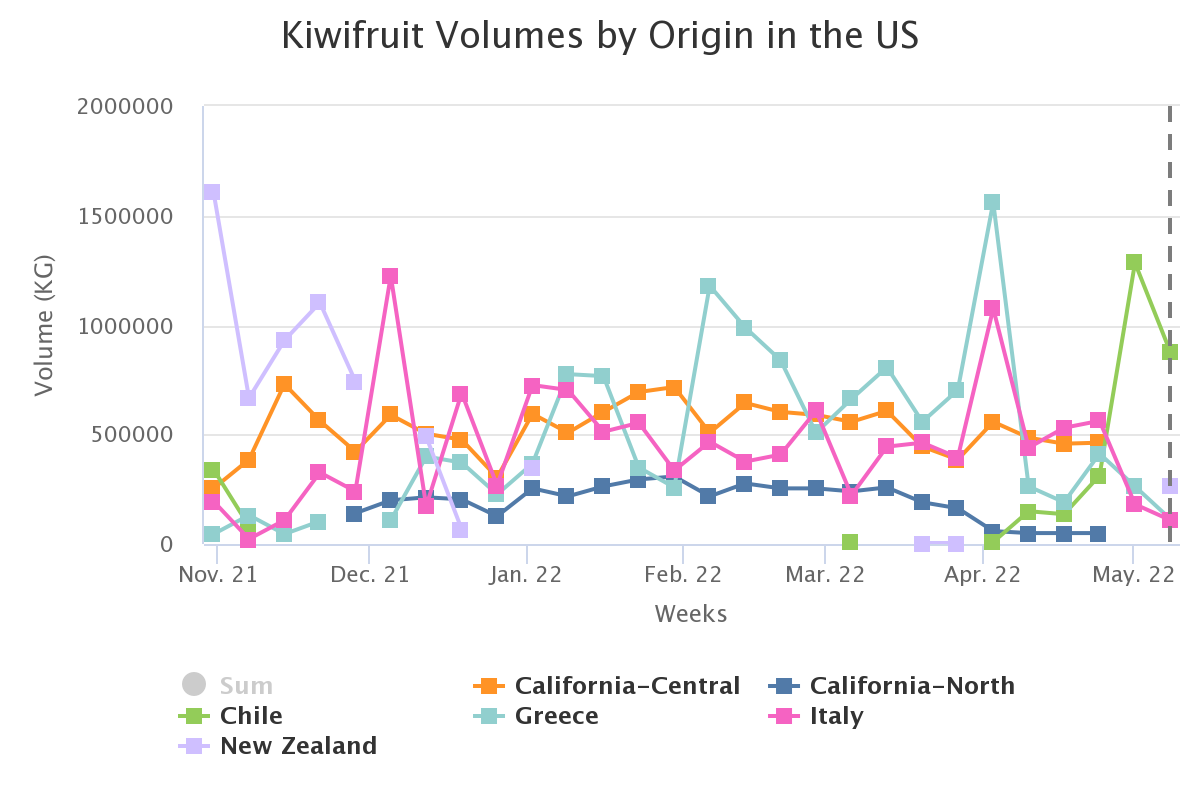

North America: Logistical issues cause back up of European fruit on market

Kiwi supplies in North America are still transitioning out of mostly European fruit.

Source: USDA Market News via Agronometrics.

(Agronometrics users can view this chart with live updates here)

“There’s still mostly Italian fruit available still because there were a lot of logistics problems getting the product into the U.S. So, it’s in clean up mode there,” says one California-based importer.

At the same time, there is also some California kiwi volume as well and New Zealand kiwis will also start this month.

The fact that there’s still European fruit in the market has in turn slowed down Chile’s kiwi start, although it has been shipping fruit for about a month. “But it’s been more limited volumes to start and a lot of that is driven by importers saying–hey, don’t send it right now because there’s clean up from the Northern hemisphere,” says the shipper.

Overall, he notes that the Chilean crop size is similar to slightly greater than last year’s crop. “It seems like the sizing is a bit smaller compared to other years and when you have smaller sizes, you generally have less tonnage, though that’s still to be determined,” he says.

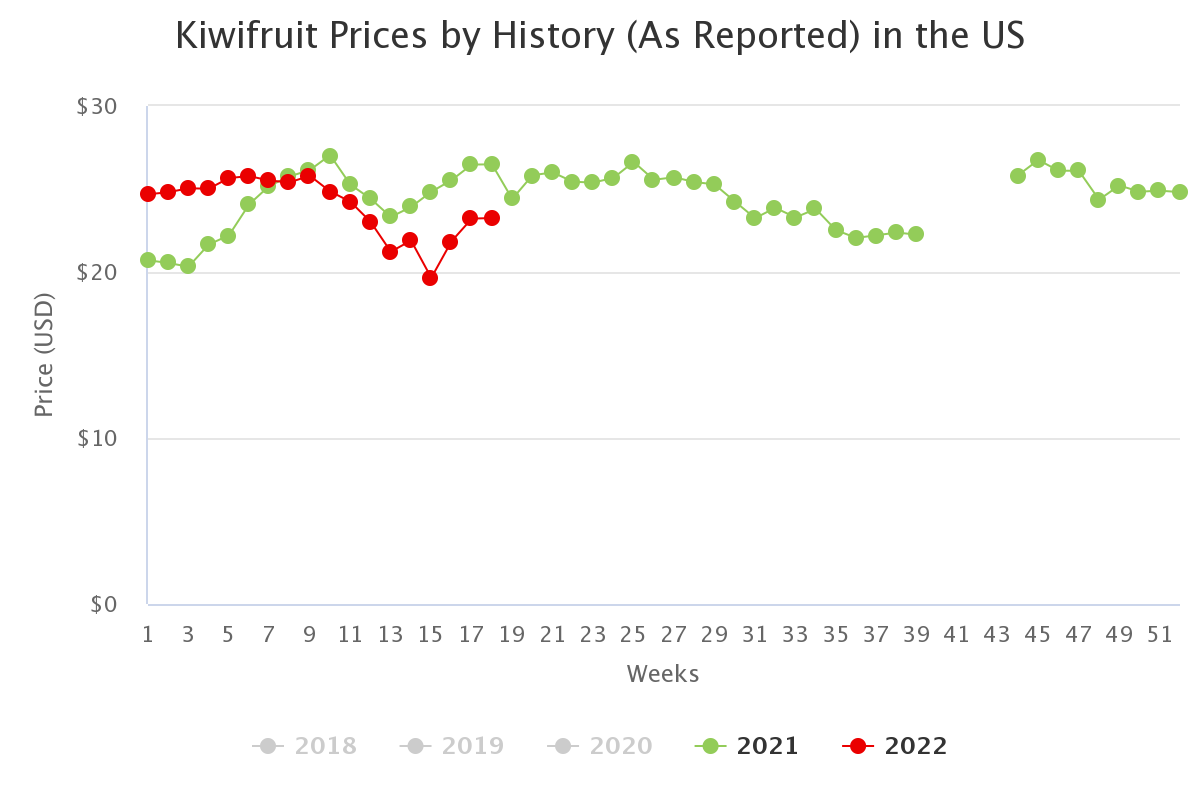

Demand and pricing have both been stable. “It’s not a huge promotion item. And for the European and the Chilean fruit, costs are higher due to many inflationary things. But if the market starts backing up and really falling behind, it’s not going to matter what the costs are at some point,” says the importer, adding that pricing is slightly up over last year. “Pricing is similar to slightly higher but under different circumstances than last year at this time. We didn’t have this much leftover fruit from the Northern hemisphere when the Southern hemisphere fruit got going.”

Source: USDA Market News via Agronometrics.

(Agronometrics users can view this chart with live updates here)

That said, he does note that while logistics are better than they were three to four months ago, they are still more difficult compared to other seasons. “That’s contributing to the back up of European fruit lingering in markets around the world. It’s caused Chile to have a slower start on exports because demand is curtailed because of that,” he adds.

Looking ahead, the transition away from European fruit will continue and demand in the U.S. is anticipated to wane somewhat. “Kiwis move a bit better while school is in session and summer break is coming up pretty quick,” he says. “Demand slows down from mid to late May and through most of the summer. So we see regular business maintaining but we don’t see an uptake in demand.”

South America: High European stocks delay start of the kiwi campaign from the southern hemisphere in Europe

Chile expects to market between 150,000 and 155,000 tons of kiwis in this new campaign; however, the start of the season has been slower than expected, since it has coincided with significant stocks of fruit in the markets in the northern hemisphere.

In fact, up to week 16, the volumes shipped by Chile to the different international markets represented only 62% of those shipped up to the same week of 2021.

“Zespri has been exerting more and more pressure on the markets to place and market its supply of yellow kiwifruit, delaying the sale of its green kiwifruit, which has meant that Europe has had to delay the start of its campaign until mid-December, when normally they should start in November”, explains an industry representative. “Starting later means having less time for marketing in the campaign, which is why Europe is trying to increase overseas shipments to try to balance supply in order to obtain a better return for its producers.”

The contraction in shipments has been driven precisely by the delay in shipments to Europe and the presence of European fruit in the destination markets for Chilean kiwis. According to data up to week 16, North America has been the main destination for Chilean fruit, receiving 35.2% of exported volumes and registering the smallest drop in shipments, only -6%. Latin America is the second most important destination receiving 25.3% of the Chilean kiwis exported (-26%), followed by Europe with 19.3% (and a notable drop of 64%), the Far East with a 14% share (-43%), the Middle East with 5.2% (and leading the only positive year-on-year variation, with +12%) and Russia, where shipments have fallen by 93% to represent a symbolic 0.6 % of the total.

“However, this slower start to the harvest has allowed the Chilean industry to have fruit with better physiological parameters, although with smaller sizes than we would like due to climatic factors.”

The News in Charts is a collection of stories from the industry complemented by charts from Agronometrics to help better tell their story.

Access the original article with this (Link)

Related Stories