Pears in Charts: Recent pricing pushed below previous years’ levels

By

| 26 February 2019

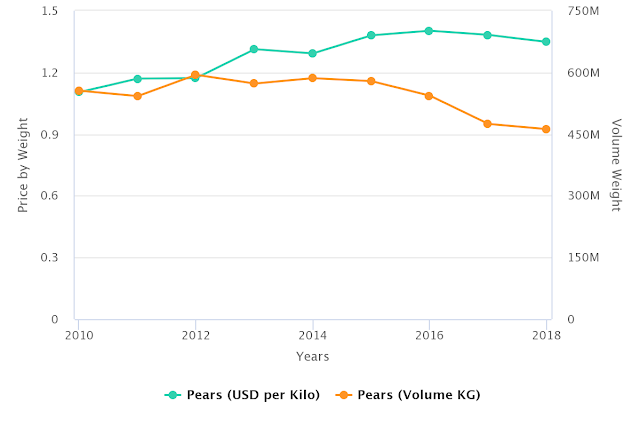

Taking a look at the pear markets, the first thing that struck me when I began researching this dataset is that the market appears to be in decline, which I haven’t found to be very common among the different commodities we work with. From the available data it seems that 2015 was pears’ best year, after which volumes began to decrease, dropping by almost one fourth since their high point of 2012.

Initially, the drop in volume coincided with increases in pricing, but that trend has since tapered off, seeing both a drop in price and volume over the last two years. This tells me that the demand for pears is waning. At the same, time other fruits are seeing growth, so it appears that consumers are choosing to spend their dollars on other products, which has been eating into pears’ market share within the produce aisle. I don’t have any objective data on what products are taking market share from pears, but any comments or opinions on the subject would be more than welcome.

Pear Non Organic Prices and Volumes

(Source: USDA Market News via Agronometrics)

[Agronometrics users can view this chart with live updates here]

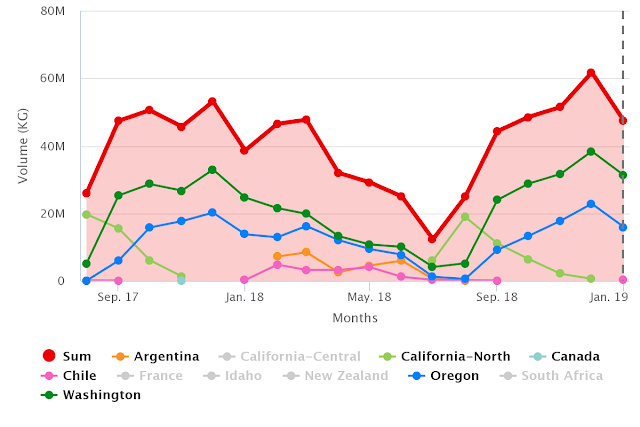

Digging a bit deeper we can appreciate the different seasons and the roles of each of the origins in the market. My focus in this article will be on Chile and Argentina, whose season is about to begin and whose exporters and their counterparts may be looking at the same data to put together their programs for the upcoming season.

Chile and Argentina roughly share the same commercial window, with Argentina far and away the largest producer in the Southern Hemisphere, sending about twice the volume Chile sends on any given year. Starting after Washington and Oregon’s peak in production, they prop up supply from February to July before Northern California gets going.

Pear Non Organic Volumes by Origin

(Source: USDA Market News via Agronometrics)

[Agronometrics users can view this chart with live updates here]

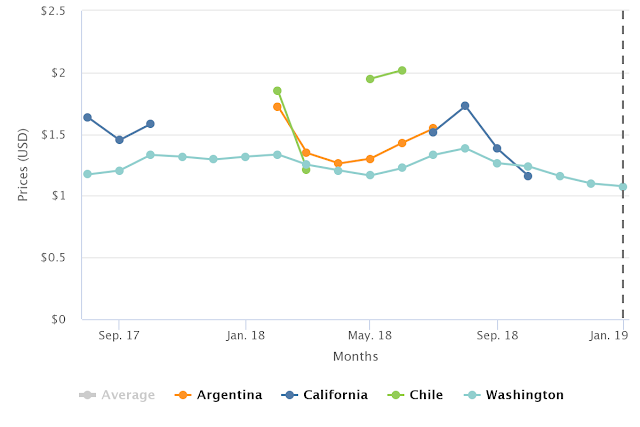

The pricing that both Chile and Argentina enjoy is typically higher than Washington’s, with Argentina historically receiving a 10% premium on Chile’s prices. Last year was a rare exception in which Chile’s prices were equivalent to or higher than Argentina’s.

Pear Non-Organic Prices per Kilo by Origin

(Source: USDA Market News via Agronometrics)

[Agronometrics users can view this chart with live updates here]

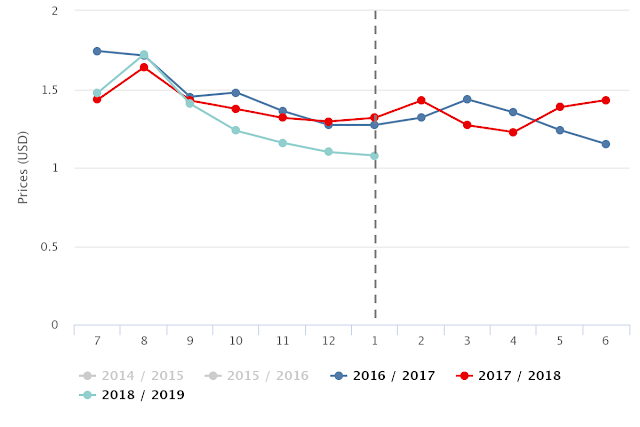

Coming in after four months of low prices, I wanted to better understand where the market is now to get a better idea of where we are going. Prices from October to January were 14% lower year-on-year. This drop has come hand in hand with a rise in volume, but only 11% year-on-year.

Historic Pear Non-Organic Prices

(Source: USDA Market News via Agronometrics)

[Agronometrics users can view this chart with live updates here]

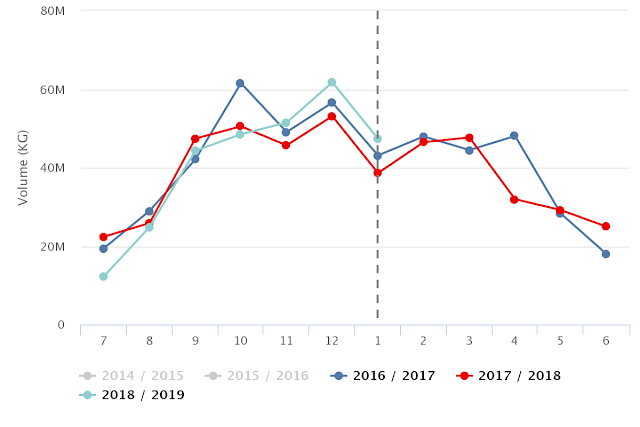

Like with most commodities, you can see that there are high volumes matching up with the low pricing of the last three months, however, October is a bit of an enigma. Looking back another two years and a trend began to form, where October has been consistently underperforming previous years with a consistent miss-match between pricing and volumes compared to the nearly all other time periods of the year. This may be something to consider producers in Oregon and Washington, where the month corresponds with the peak of production.

Looking forward, everything I can find in the data indicates that the next couple of months shouldn’t hold any big surprises, where changes in volume compared to last year should be proportional to changes in pricing compared to last year. The only exception might well be April, which has also seen big changes in volume without reflecting changes in pricing.

With a 4% year-on-year increase in production forecast for both Chile and Argentina season (Mixed picture for Southern Hemisphere pome fruit production), I would expect prices to come up a bit over the next couple of weeks, but as long as Oregon and especially Washington continue to deliver the large volumes we have been seeing. The pricing we have seen from Chile last week already seems to be an improvement on last year, coming in at $0.54 higher for 18 kg cartons tray pack.

Historic Pear Non-Organic Volumes

(Source: USDA Market News via Agronometrics)

[Agronometrics users can view this chart with live updat

es here]

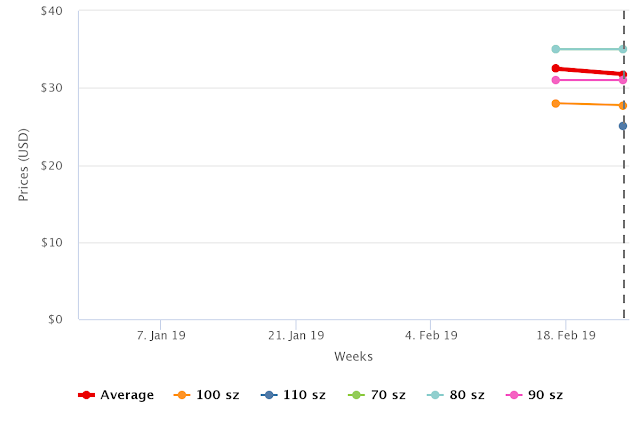

As a useful tool for readers to gauge how the markets are currently evolving, we offer weekly pricing by fruit size.

Pears, Summer Bartlett, Non Organic, Prices by Size

(Source: USDA Market News via Agronometrics)

[Agronometrics users can view this chart with live updates here]

Pears, Summer Bartlett, Non-Organic, Prices by Size (Week 8)

| Sizes | Price Reported |

| Average | $31.76 |

| 70 sz | $35.00 |

| 80 sz | $35.00 |

| 90 sz | $31.00 |

| 100 sz | $27.75 |

| 110 sz | $25.00 |

Written by: Colin Fain

Original published in FreshFruitPortal.com on February 26, 2019 (Link)