Pears in Charts: USA Pears CEO on two interesting factors this season

By

| 17 September 2019

In response to the article we wrote a couple of weeks ago, I spoke to Kevin Moffitt, the President and CEO of USA Pears. He had some more insight about the upcoming pear season, which I wanted to share with our readers in this week’s In Charts installment.

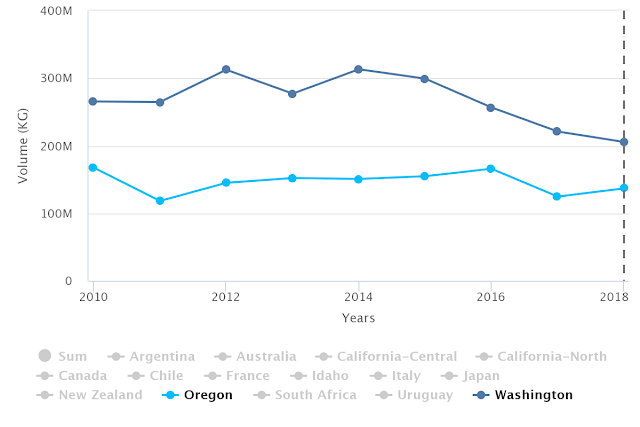

Because the last article focused on the Washington market data, Kevin was prompted to mention that the Hood River district, in Oregon, is forecasting more pears than the Wenatchee district in Washington – the first time this has happened in many years. Washington, however, will still put up the largest numbers overall.

From the standpoint of a market analyst, this is an interesting development, we don’t know if the switch between Hood River and Wenatchee will be a one time event or not, but it does seem to reinforce the downward trend that has been observed in Washington fruit over the last five years against an increased market share for Oregon.

Non-Organic Pears Volumes Sold on the Domestic Market by State of Origin

Source: USDA Market News via Agronometrics. (Agronometrics users can

view this chart with live updates here)

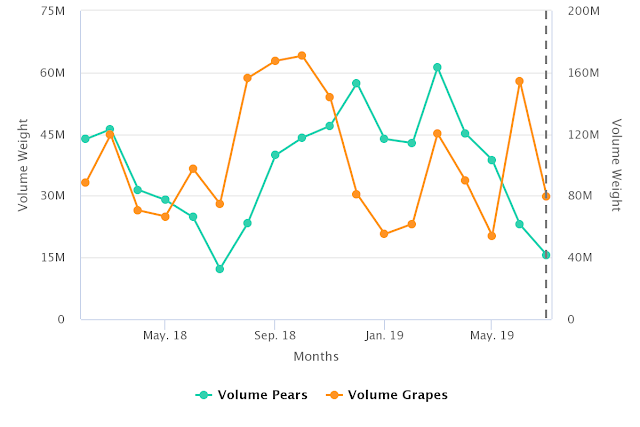

Another important item that Kevin mentioned based on the previous article was the possible effect that a strong grape season could have on pear prices.

I pulled the data to create the chart below comparing grape volumes next to pear volumes. Considering grapes commercialize about three times the volume of pears, we set them on different axes to show where the crops overlap. The biggest impact that grapes could have on pears should be towards the beginning of the season in September, October and November – at the height of the U.S. grape season, as pears come online.

Last year California grapes had a banner season, greatly oversupplying the market and pushing down prices. We wrote a more in-depth analysis of this last month in our Grapes in Charts article.

Kevin believes that the grapes made a complicated pear market tougher. They flooded grocery store shelves and took a larger percentage of ad space for promotions, leaving less room for pears. What’s more, rock bottom prices for grapes make an attractive purchase for clients, and “at the end of the day how many pounds of fruit will people really purchase, although they should eat much more fruits and vegetables”.

With Grapes expected to be 3% down on last year’s crop, the relationship between these two commodities will be an interesting one to follow.

Non-Organic Pear and Grape Volumes

Source: USDA Market News via Agronometrics. (Agronometrics users can

view this chart with live updates here)

Written by: Colin Fain

Original published in FreshFruitPortal.com on September 17, 2019 (Link)